JSMedia – How Will COVID-19 Affect Mortgage Lenders’ Loan Processes? Lenders have tightened their requirements following the coronavirus outbreak, but this may not affect you. It could have been the high unemployment rates that forced lenders to tighten their standards. If you’ve been in the market for a mortgage, you can expect to have to pay a bigger down payment.

When applying for a mortgage, the lender will check to see if the process is affected by COVID-19. Several steps are involved in the process, including title searches, appraisals, employment verification, income verification, notarization, and closings. Lenders will be able to process your loan if they have their systems set up to withstand the virus. If a county recordation office is closed, your mortgage application cannot become official. In some areas, lenders will have a ‘workaround’ system that can work in Coronavirus, but other areas will not.

A COVID-19 forbearance period is designed to help homeowners recover financially. However, this can lead to missed mortgage payments. A private sale is a standard transaction where a property is sold at a price that pays off the loan in full. If the borrower cannot make his payments during the forbearance period, the mortgage loan may be resold to Fannie Mae or Freddie Mac.

How Will COVID-19 Affect Mortgage Lenders’ Loan Processes?

A COVID forbearance is a temporary suspension of payments. Under this plan, the mortgage company agrees to accept reduced or no payments for a specified period of time. During this time, interest and other penalties will continue to accrue. In contrast, a CARES forbearance is specific to the CARES Act. Both COVID forbearance and CARES act forbearances have similar conditions.

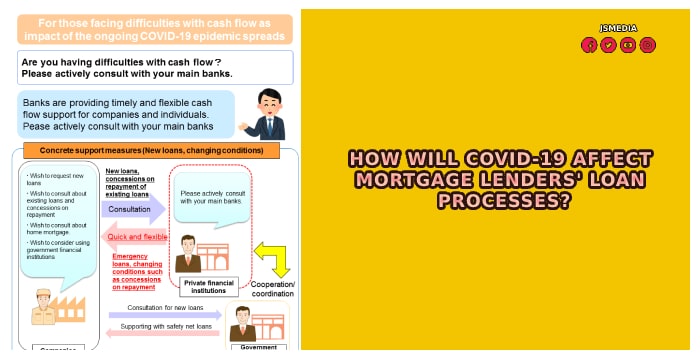

Currently, COVID-19 has largely affected how mortgage lenders handle their loan processes. Since the statutory funding fee has increased, borrowers whose loans were affected by severe storms are ineligible for a payment deferral. If you have an existing modification, you may want to wait until the new regulations come into effect. If you’re a VA home loan borrower is impacted by COVID, you should consider seeking an extension.

When COVID-19 is implemented, it has also affected loan servicing. This means that you must report the delinquency status information in the Servicing Solutions System to the federal government. As a result, lenders will have to update their loan processes to make sure they’re in compliance with the new requirements. If the borrower’s loan has been in delinquent for a year, he will be eligible for a payment deferral.

Moreover, COVID-19 affects servicing. If you need to apply for a mortgage loan, the best option is to request an extension. If you’re in need of an extension, you can submit an application for one. It’s not uncommon for a servicer to request an exception for borrowers affected by disasters. If you need to, you can also ask the lender for a delay.

If you’re in need of a mortgage, you can ask your mortgage company to grant you a hardship forbearance. This is a great way to get a mortgage in the current economic climate. This way, the mortgage company will have time to work out the problems with the loan and allow you to get back to your regular monthly repayment schedule.

Aside from its impact on the mortgage industry, it can affect the economy. The FHFA closely monitors the coronavirus as a national emergency. This is why the agency has updated its policies and guidance. The FHFA is also working to make sure the process is simple and convenient for consumers. Its main goal is to ensure the stability of the country’s economy.

When COVID-19 came into effect, lenders tightened their lending standards to avoid the possibility of further foreclosures. In addition to tighter credit standards, the Department of Justice has launched criminal and civil enforcement efforts against fraudulent mortgage schemes. The DOJ announced a number of schemes involving the Paycheck Protection Program, the Unemployment Insurance program, and the Economic Injury Disaster Loan programs. As a result, the DOJ has increased their efforts to combat this fraud.