JSMedia – In a recent survey, the Mortgage Bankers Association reported that 52% of mortgage lenders predicting that profits would decrease in the next three months. This is in contrast to the 48% who said that their profits would rise. In the survey, the respondents also said that the demand for both refinance and purchase mortgages will increase. Furthermore, they said that the rising job security and mobilization of vaccines will boost consumer confidence.

Despite the negative news for investors, mortgage lenders continue to expect good profits in the coming quarters. During the second quarter of last year, demand for all loan types increased by 4 percent. In August, the average primary mortgage spread was 229 basis points, which is higher than the long-run average of 170 basis points. Lenders are also expecting the same profit margins in the next three months.

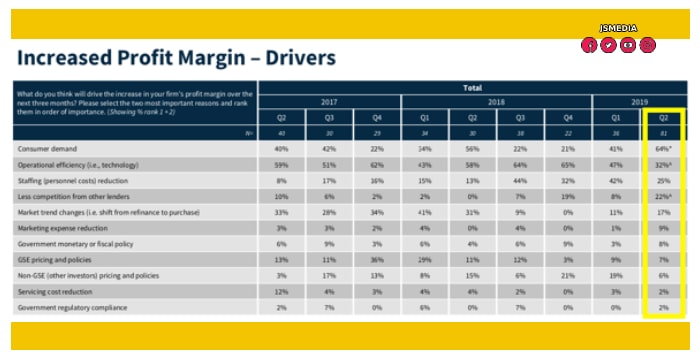

While the survey results indicate that mortgage lenders are predicting profit drops in Q2, the good news is that the results of the survey indicate that profits are likely to remain strong. Lenders are also citing competition from other lenders and a shift from refinancing to buying. While these results are concerning, they do not necessarily mean that mortgage lender profits will fall this quarter. The next quarter’s results are not yet final, so investors should consider the latest trends before making their next investment decision.

Mortgage Lenders Predicting Profit Drops in Q2

The current economic picture is improving and putting upward pressure on mortgage rates. 30 year fixed-rate mortgage rates are already nearing 3%. The Mortgage Bankers Association (MBA) forecasts that the Freddie Mac survey rate will reach 3.5% by the end of 2021. The rise in interest rates has been a boon to the industry, but it will be tough to sustain profitability. It’s time for lenders to become more efficient, creative, and resilient to margin compression.

The changes in the mortgage market are expected to continue to hurt the industry. While the mortgage industry has always been a profitable one, the market is becoming more competitive and more difficult for lenders to remain profitable. This is why mortgage bankers are looking to find new ways to grow their businesses. In addition to being more competitive, these changes will also mean that interest rates will decrease. In turn, it will make it harder for them to compete in the marketplace.

While the overall consumer demand for mortgages has remained strong and topped record highs, mortgage lenders continue to report that they are still seeing significant gains in purchase mortgage demand. In addition, the demand for refinances remained strong, despite the tightening of credit standards. Despite the negative news for home buyers, many consumers are still hopeful that the market will recover. This will allow them to enjoy a higher standard of living.

Lenders should focus on preparing for the coming recession. By implementing these measures, mortgage lenders can protect themselves from these losses. In particular, they should make sure that they have a strong financial buffer, which can reduce their risk of defaulting. In the event of a recession, their profits will fall. And while they should still continue to operate at their current levels, they must also adapt to the new circumstances in the mortgage market.

In addition to these challenges, the latest survey results also reveal positive news for both lenders and homebuyers. The survey asks lenders whether they think prices will rise or fall over the next twelve months. In January, the number of eligible homeowners was at 18 million. By November, the number fell to just over 12 million. The percentage of homeowners eligible for refinancing dropped by 30% in a month.

While the survey results are good news for homebuyers and mortgage lenders, the outlook for the housing market isn’t as bright as many think. The median 30-year fixed mortgage rate will drop to 2.87% by the end of 2021, which will lead to a slowdown in the refinancing boom. By contrast, the average rate for a refinanced mortgage will drop by more than half in 2021.