JSMedia – A recent survey from Fannie Mae found that margin compression is likely to become worse this year. Lenders who have aggressive marketing and sales efforts may fare better during the current recession, despite the fact that their bottom line will be affected. This is because lenders who have a high retention rate will have more staying power and have more discretionary funds to reduce costs. Consequently, these lenders may be able to survive the current downturn.

Lenders have cut back their profit margins due to decreased demand. Since the mortgage industry is struggling with low demand, they have been forced to cut loan processing fees to remain competitive. This has affected their profit margins. The mortgage market will continue to be challenging, with fewer opportunities for mortgage executives than in the past. Additionally, new government regulations have forced many lending organizations to make drastic changes in workflow and technologies.

Lenders have lowered their interest rates to maintain profit margins, which is causing them to cut back on marketing. In addition, they are less likely to adopt innovative marketing strategies, which means fewer opportunities for mortgage executives. Meanwhile, newer government regulations have also been a major challenge for the mortgage industry. These regulations have led to a major change in technology and workflow for many organizations.

How Profit Margin Compression Affects Mortgage Lenders

Fortunately, profit margin compression has not caused all lenders to become bankrupt. The average mortgage loan portfolio fell to historic lows in the aftermath of the housing crash. In fact, more than half of all new mortgage loans will be refinances. While the industry is largely focusing on refinancing the debt of mortgages, lenders have been slow to ramp down production capacity and remain profitable.

Because of margin compression, many small banks and credit unions have had to diversify their portfolios to offset the problem. Even credit unions have been slow to ramp down production capacity, and this has forced them to lower their NIM. In addition, borrowers have more information than ever before. This can lead to more competitive pricing and increased risk for smaller community banks. Therefore, it is essential to understand how profit margin compression affects mortgage lenders.

Several economic factors are driving profit margin compression in the mortgage industry. As a result, the average profit margin of independent mortgage banks has fallen to the lowest level in two years. The fall in interest rates is largely due to the fact that lenders’ profits have been falling for the past two years. In order to survive the current recession, lenders must improve operational efficiency. However, this is not easy.

In the current mortgage market, profit margin compression is driven by multiple factors. A lack of home sales and interest rates are driving lower home prices, despite the fact that a higher mortgage interest rate can increase the amount of revenue a lender makes. Nevertheless, lenders are finding ways to minimize this pressure and maximize their bottom line. Lenders must develop a strategy to address the issue.

The overall mortgage origination volume fell by 20% in the fourth quarter of 2017, compared to 19% a year earlier. As a result, mortgage lenders reported a negative profit margin for Q1 2018. The reasons for this trend were cited as aggressive competition, lower consumer demand, declining interest rates, and increased operational costs. The market has also changed since the last recession. While some factors may have caused the decrease, the recession has affected all companies in the industry.

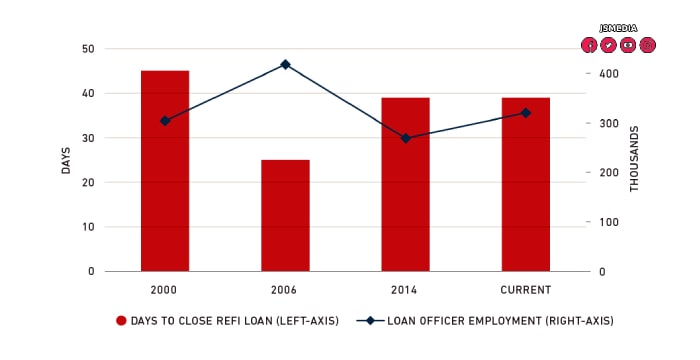

Another key element that can affect mortgage lenders’ profitability is low loan volume. The MBA Refinance Index, which was started in 1990, shows that loan volume has declined by nearly 50 percent. The current decline is the lowest percentage since the fall of 2008. Increasing rates will not fix margin compression problems in a soft market, but they can make your business more efficient. So, how do you handle this situation?