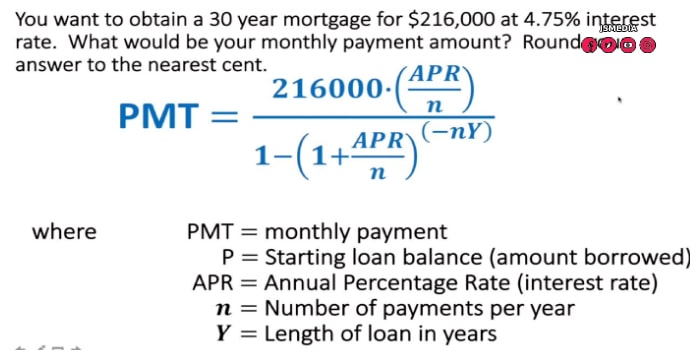

JSMedia – When it comes to determining mortgage payments, a lender will calculate the total cost of the loan based on the annual interest rate. To determine your monthly payment, the first step is to determine your gross income. This number will be based on your gross income. In addition, the monthly payment you make will include the cost of your down payment and any other expenses you incur each month. Once you’ve entered these amounts into the calculator, you will be presented with your total monthly payment.

The total cost of your mortgage loan is calculated by dividing the annual interest rate by 12. This number will represent the total amount of interest paid. In addition, the monthly payment includes any taxes and homeowner’s insurance. If you’d like to make larger monthly payments and pay off your mortgage sooner, you should consider a 15-year mortgage. The 15-year loan typically has a lower interest rate and lower monthly payments, but you may be better off with a shorter term.

In addition to interest costs, lenders also charge upfront fees. In addition to interest, your monthly payment will include any fees that are required for escrow, which are typically taxes and homeowner’s insurance. The total cost of your mortgage loan will be based on these fees. Your mortgage payment will be determined based on your total escrow payments. Depending on the amount of down payment you can afford, you can choose a shorter term.

How Do Mortgage Lenders Calculate Monthly Payments?

In addition to the interest, you must also account for annual expenses. The annual charges are usually charged in a lump sum and are paid once a year. Divide these by 12 and your monthly payment is rounded up to the nearest dollar. These costs, however, will affect the total cost of your mortgage loan. You must also remember that these costs are just a fraction of the total amount. Your actual cost of your mortgage loan will depend on other factors such as your credit history and income.

In order to calculate your monthly payment, you must know your current income and debt. The total of your debt is your total income minus the annual expenses. Once you’ve determined your income, you can add these expenses to your mortgage. A loan with a lower interest rate will require higher payments. If you have a large down payment, you can reduce the total amount of your mortgage by 20%. A down payment of at least twenty percent will eliminate the private mortgage insurance.

Besides the interest and principal, you must also consider other costs that are associated with your mortgage. Real-estate taxes can add up to a significant portion of your mortgage payment. Other expenses include insurance. These are included in your mortgage payment because they are part of the property’s value. Once you’ve decided to buy a home, you’ll need to calculate the total cost of the loan. You must figure out the cost of the loan and calculate the monthly payments accordingly.

Using a mortgage calculator is one of the best ways to determine how much you can afford to pay each month. The mortgage rate and interest rates can change throughout your mortgage term. This can affect your monthly payment. Fortunately, there are many ways to calculate your payments based on these factors. You should always consult your lender if you’re not sure how to calculate your payments. If your income is less than your expenses, you can use the DTI calculator to see how much you will pay each month.

Before looking for a home, determine how much you can afford to pay. You’ll want to make sure that your monthly payments don’t go over your income. A home that requires a higher payment than you can afford will cause you to feel stressed and unable to save. You’ll also want to consider the other costs associated with owning a home. Once you’ve decided, you can start the mortgage application process.