JSMedia – A new federal law is making it easier for lenders to lend to C-PACE projects. The program combines tax credits and utility rebates. It also works well with state incentive programs and bond financing. In addition, C-PACE allows the sponsor or senior lender to pass on the savings from the project to its commercial tenants and hotel guests. This can be an extremely valuable feature for both parties.

One of the advantages of C-PACE financing is that it is a non-recourse, long-term loan. This means that homeowners and property owners don’t have to worry about accelerating the payments. Another benefit is that C-PACE financing has minimal covenants and guarantees. Furthermore, the improvements make the property healthier, more comfortable, and more valuable to future owners.

In addition to these advantages, C-PACE loans have certain risks. Since the assessments are not accelerated, the risk of a borrower defaulting on the loan is reduced. Because the lender is more likely to foreclose than a conventional mortgage lender, it is crucial for lenders to carefully evaluate C-PACE loan assessment data to assess the risk of loan default. As a result, underwriters should look for C-PACE loans when reviewing title reports and drafting loan documents.

Mortgage Lenders C-PACE Financing, You Can Prove You Can repay The Loan

Another benefit is that C-PACE financing is tied to the property. This means that the property remains tied to the loan even if the owner of the building changes ownership. It is also important to note that the loan is tied to the property. This means that if the owner decides to sell the property, the loan will stay with the property. It is important to remember that if you can prove you can repay the loan, C-PACE financing is an excellent option for you.

While the program requires the consent of the mortgage holder, mortgagees may consider collaborating with a CPACE borrower. In many cases, the lender will be reimbursed for their losses if a CPACE lien is placed on the property. In addition, a CPACE project will reduce the homeowner’s property taxes. The benefits are obvious. The new financing option will help homeowners pay their bills.

While C-PACE financing may not be suitable for every project, it can offer the developer with a low-cost alternative to a traditional mortgage. In addition to saving money on monthly payments, CPACE finance will allow developers to install LED lighting, energy-efficient plumbing, and improved insulation. All these improvements will save energy and lower the property’s monthly maintenance costs. In addition, the CPACE loan will not be paid off until all the units are leased.

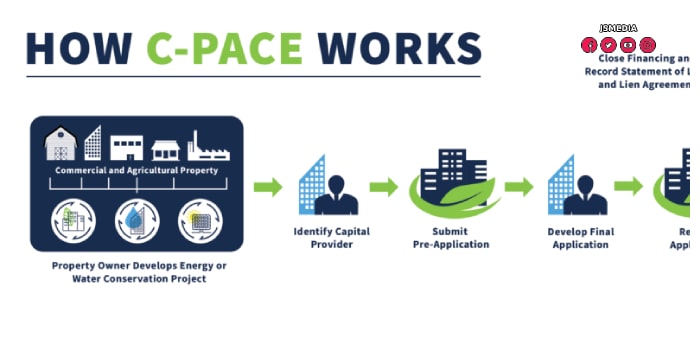

The approval process for C-PACE financing is much more relaxed than for a conventional mortgage. A property owner can finance 100% of the cost of energy-related improvements. A lender’s creditworthiness is not a major factor in the approval process for a C-PACE loan. The program is administered by state and local government agencies, and the guidelines are set by these governments.

CPACE financing is currently legal in over 30 states and continues to grow. This program allows building owners to borrow money for energy-efficient upgrades, and in many cases, it has enabled borrowers to pay their property taxes. In addition, C-PACE financing can be used for renovations as well as for new construction. In most cases, borrowers will be able to use the funds to pay for their improvements.

A PACE loan may be in place at the time of mortgage loan origination. It is a form of financing that allows building owners to use a portion of the loan to finance renewable energy installations and energy efficiency improvements. The program works similarly to a property tax assessment, and requires a completed application form. For more information, contact C-PACE. This program is intended for commercial properties, but it is not applicable for residential properties.

There are several benefits to C-PACE financing. The loan has a low interest rate and is non-recourse. In addition, it does not encumber the property. In the event of default, the loan is non-recourse and stays attached to the property after sale. It is therefore an attractive option for both homeowners and lenders. Unlike many mortgage programs, C-PACE financing does not require a down payment or any closing costs.