")

JSMedia – Lenders mortgage insurance is a policy that protects the lender when a borrower fails to make their payments. This insurance premium is added to the loan amount. The higher the percentage of the loan, the more mortgage coverage you will need to pay. Depending on the lender and the size of the deposit, the cost of LMI can vary considerably. The average cost of LMI is several thousand dollars.

LMI is designed to reduce the risk to the lender, which is important for people with smaller deposits. It is also ideal for first-time buyers, who may not have enough money to deposit a large amount of money. However, a larger deposit will take many years to accumulate, and a small deposit will require assistance from family and friends. LMI helps people buy homes sooner, despite their limited financial resources.

Lenders mortgage insurance is an insurance policy that covers the lender. The borrower is the beneficiary, and the lender is the one who pays the premium. The lender benefits as the insurance provider will try to recoup the shortfall amount from the borrower. The downside to LMI is that it costs borrowers money upfront, so it’s important to understand the risks before applying for it. This type of insurance is not for every borrower. The upfront cost is usually higher for first-time borrowers, so it’s worth knowing how much to budget for.

Lenders Mortgage Insurance, Should Help You

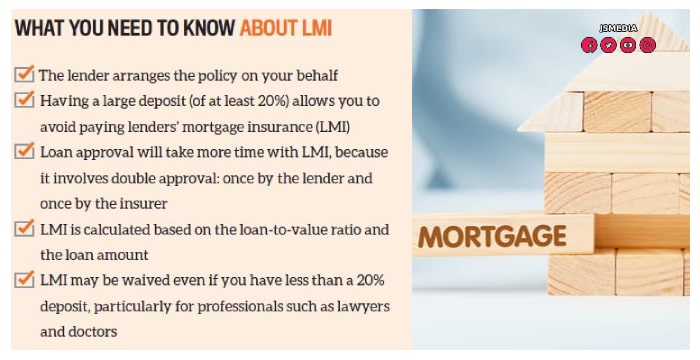

LMI can be a major part of the total home loan. If you plan on putting 20% down, it’s best to get licensed financial advisers to help you determine the costs associated with your loan. It may take longer to get your loan approved, but the extra time is worth it. Your lender will also require additional requirements from your assigned insurer. These will add to the length of time it takes.

LMI is a type of mortgage insurance that protects the lender from default. It is not a loan, but a mortgage insurance premium is paid up front. This is a refundable premium. But it’s best to avoid refinancing your loan and waiting for the deposit to increase. If you can’t afford to pay LMI, you can always wait. Otherwise, you could end up paying more than you should.

LMI protects the lender. If you fail to make the payments on your loan, LMI will protect the lender. If you default on your loan, your lender will need to sell the property to cover the shortfall amount. In this case, LMI doesn’t protect the lender. If the borrower defaults on his or her loan, the insurer may pursue you for the shortfall. The lender’s insurance company is liable for the shortfall.

LMI protects the lender from loss if you default on your loan. Its value is directly related to the amount of money you borrow, and the bigger the loan, the higher the cost of LMI. While LMI costs vary between providers, you can choose a provider that suits your budget. The premium cost for LMI depends on the lender and the type of mortgage you take out. If you are in a high-paying industry, you can borrow up to 90% of the value of the property.

LMI is a cost that lenders require from you when you apply for a mortgage. It is an upfront fee that will be added to the loan over the course of its life. LMI is a good option if you have a small deposit, but it will cost you more money in the long run. You can pay the lender at the time of settlement or when you settle the loan. When settling, you can negotiate the terms and conditions of the mortgage.

LMI costs vary from lender to lender. Smartline Advisers can give you more information about LMI costs. Typically, a 20% deposit can avoid LMI. The cost of LMI is only about a third of the total loan amount. It can be avoided with a 20% deposit, or by lowering the loan to value ratio. A lower LTV will reduce the cost of LMI.