JSMedia – Before you start comparing mortgage lenders, you need to decide what type of loan you want and what features you need in a mortgage. Then, you can contact multiple lenders and gather all of the relevant information. Make sure you compare the total cost of the loan, including points, fees, and closing costs. If you are unable to do this yourself, you can consider hiring a mortgage broker to help you. However, keep in mind that the broker will charge a fee.

It is important to note that different lenders may offer dramatically different interest rates and terms. These differences can be caused by varying risk policies and business models, which mean they will charge different fees and interest rates. It is crucial to compare mortgage rates and fees to ensure that you are getting the best deal possible. The easiest way to do this is to get the loan estimates of several different lenders. This will help you identify the lowest rate, as well as the terms and upfront costs.

Once you’ve narrowed down your initial list of lenders, it’s time to compare the various loan offers. You can look at their interest rates, terms, and costs, as well as their relationship and comfort level. In addition, you should look at the upfront fees and costs that lenders charge. By comparing interest rates, fees, and terms, you can find the best mortgage loan for the most competitive price.

How Do You Comparing Mortgage Lenders?

To compare mortgage rates, it is best to look at the total amount that you’ll be paying over the life of the mortgage. Many borrowers will keep their mortgage for five years, so you’ll want to calculate how much you’ll pay in five years. This information is located in the Comparisons section of the website. After obtaining a preliminary quote, LendingTree will contact up to five lenders.

Most borrowers will keep their mortgage for at least five years, so the amount of money they spend will be very important in the long run. If you’re planning to pay off your mortgage after five years, then you need to calculate how much money you’ll pay in that time. Most of the time, you’ll end up paying less than you initially borrowed. But, if you can get a lower interest rate, you’ll be happy with it.

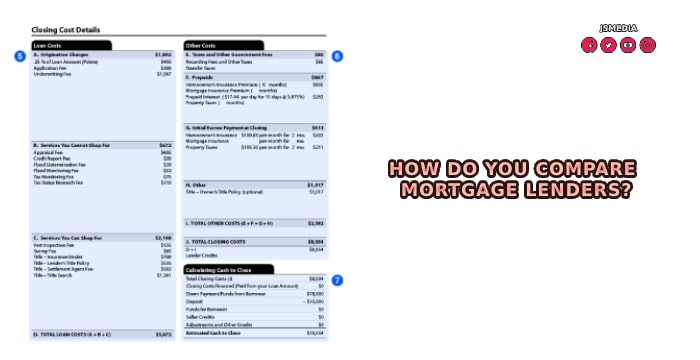

APRs and fees are also important to look at when comparing mortgage loans. APR is the effective interest rate (the rate plus any closing costs) that you will pay over the life of the loan. If the APR is too high, it’s worth negotiating with the lender to lower the amount of fees. But, this is not the only way to compare mortgage rates. You should be careful about the costs. You want to pay for the entire mortgage.

You should be sure to compare mortgage rates from several lenders before committing to a mortgage. Always remember that the best mortgage rates are the ones that fit your financial needs and credit score. By comparing mortgage rates, you can find the best mortgage rates and fees for your needs. You can also use a mortgage rate comparison tool to get an idea of what you can afford. You can also consult with your broker regarding your credit history.

While mortgage rates are the most important part of a mortgage loan, you also need to consider the costs of the mortgage. Interest rates can fluctuate daily, so it’s a good idea to monitor the trends of the market. By comparing multiple quotes, you can determine the best mortgage rate. Then, you can negotiate with the lender to reduce the fees and interest rates. If your finances are not sufficient, you can still try to negotiate for a better deal.

Compared with the other lenders, the interest rates of some of them are the most important. Some lenders offer lower rates with lower fees, while others charge higher rates with lower fees. If you can get the best mortgage rate for you and your budget, it’s time to negotiate with your lender. As long as you understand the details of the loan, you can make the best decision. It’s a good idea to compare several different quotes before deciding on a mortgage.